CANADIAN NATIONAL RAILWAY (CNI)·Q4 2025 Earnings Summary

CN Rail Beats Q4 as OR Hits 60.1%, But Stock Slides on Muted 2026 Outlook

January 30, 2026 · by Fintool AI Agent

Canadian National Railway delivered a strong Q4 2025 with EPS beating consensus by 3.3% and revenue edging estimates by 0.3%, but shares fell 2.8% as management provided cautious 2026 guidance expecting flattish volumes amid persistent tariff uncertainty . The railroad posted its best quarterly operating ratio of the year at 60.1%, a 250 basis point improvement year-over-year, driven by productivity gains across labor, locomotives, and fuel efficiency .

Did CN Rail Beat Earnings?

CN beat across all key metrics in Q4 2025:

*Values retrieved from S&P Global

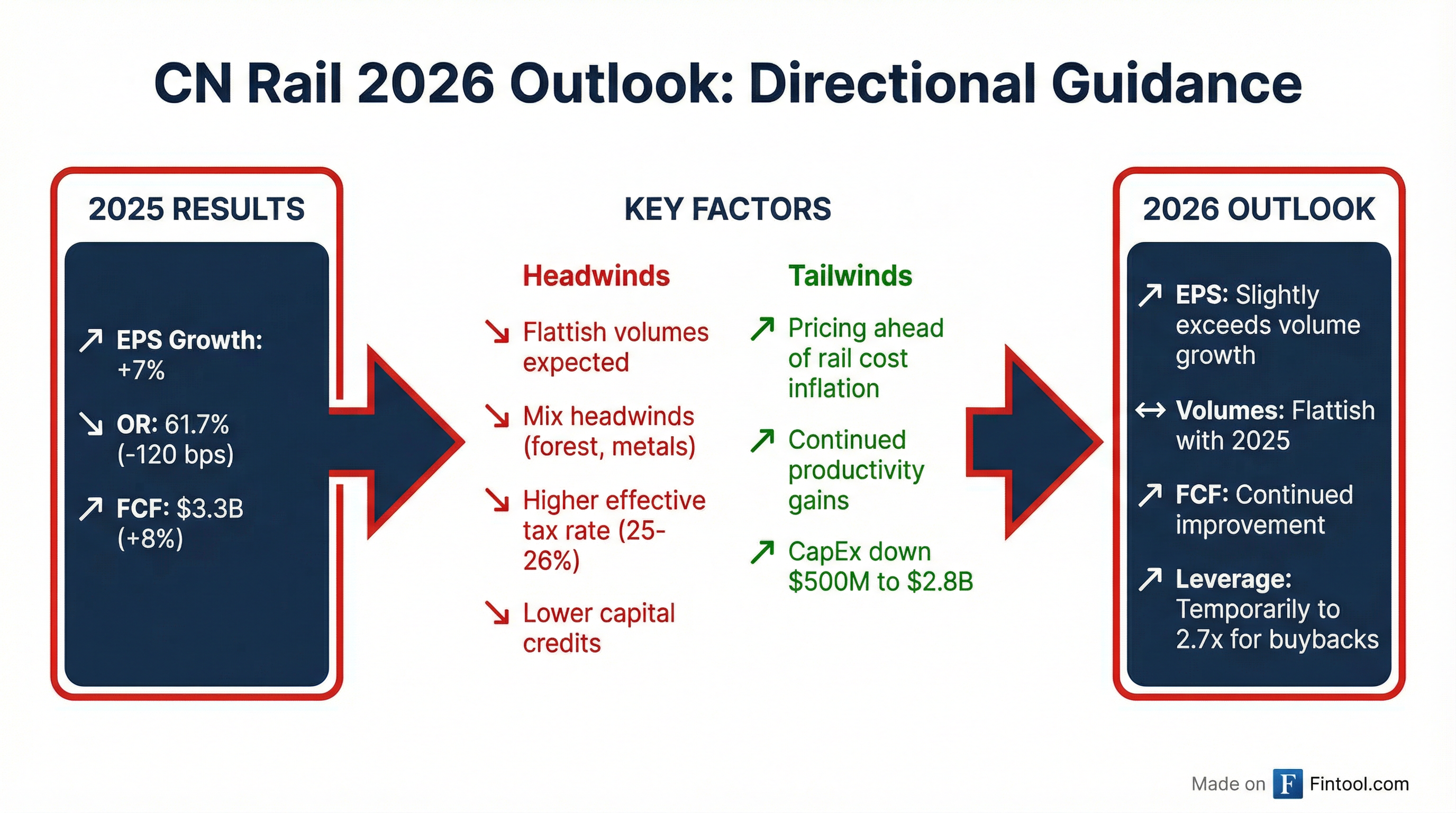

For the full year, CN delivered adjusted EPS of $7.63, up 7% year-over-year and at the high end of their mid-to-high single-digit guidance range . Full-year operating ratio improved 120 basis points to 61.7%, while free cash flow reached $3.3 billion, up 8% .

What Did Management Guide for 2026?

CN shifted to a "directional guidance" framework given elevated macro uncertainty, particularly around tariffs and the USMCA review :

2026 Key Assumptions :

- Volumes: Flattish with 2025 (assumes current tariff levels persist)

- EPS: Growth to slightly exceed volume growth

- CapEx: $2.8 billion (down $500 million from 2025)

- Leverage: Temporarily increasing to 2.7x from 2.5x for buybacks, returning to 2.5x in 2027

- Effective Tax Rate: 25-26% (vs 24.7% in 2025)

- FX: Neutralized at 71.5 cents (every penny move = ~5 cents EPS)

CEO Tracy Robinson emphasized this directional approach reflects the reality that "volumes aren't growing, so earnings aren't really growing" in the current environment, but stressed the company is building "an engine with strong operating leverage" that will accelerate when volumes return .

Notable Headwinds :

- Lower capital credits (~$100 million impact) due to smaller CapEx program

- Higher effective tax rate (~$100 million impact)

- Lower other income (2025 included ~$100 million in gains)

- Continued unfavorable mix from weak forest products and metals

What Changed From Last Quarter?

Improved:

- Q4 operating ratio of 60.1% vs 61.7% full-year (best quarterly OR of the year)

- T&E labor productivity up 14% year-over-year in Q4

- Locomotive productivity up 5% with 92.5% availability (all-time high)

- Record Q4 fuel efficiency

- Grain volumes set monthly records in October, November, and December

Deteriorated:

- Forest products "continued to deteriorate even since last quarter with some additional mill closures or curtailments"

- January volumes showing Q1 will be "the toughest quarter on a year-over-year comparable"

- Tariff impacts exceeded $350 million for full-year 2025

- International intermodal "pretty slow right now" and expected to continue into Q2

Key Management Quotes

On the Operating Environment — CEO Tracy Robinson :

"Against that backdrop, we believe a more directional framework for guidance tied to volume trends makes sense. Given what we see today, our base case expectation is that volumes will be flattish with 2025. It's important to note that at this time, the most reasonable approach is to assume that current tariff levels stay where they are."

On Operating Leverage — CEO Tracy Robinson :

"If you think about mid-single digit volume growth, with the cost structure that we've built and are continuing to build, you can see us generate double-digit EPS."

On Capital Returns — CFO Ghislain Houle :

"Our board has approved a 3% increase in CN's dividend, marking the 30th consecutive year of dividend growth. We're temporarily going to increase our leverage from 2.5 times to 2.7 times. We want to take advantage of the cheap share price."

Segment Performance

Winners :

- International Intermodal: +13% (favorable comp vs 2024 port labor disruption, Gemini service gains at Prince Rupert)

- Domestic Intermodal: +6% (service-related market share gains)

- Natural Gas Liquids: +9% (strong domestic demand, export strength through Prince Rupert)

- Grain: Record annual Western Canadian grain shipments, monthly records in Q4

Challenged :

- Forest Products: Weak demand, elevated tariffs and duties, mill closures

- Metals & Minerals: Lower iron ore (weak fundamentals, mine closure), weak frac sand demand

- Thermal Coal: Persistently weak U.S. export demand

How Did the Stock React?

CN shares fell 2.8% on the earnings release, trading down to $98.23 from the prior close of $101.03. The stock is now:

- 9.6% below its 52-week high of $108.75

- 8.3% above its 52-week low of $90.74

- Roughly flat with its 200-day moving average of $98.24

Why the selloff despite the beat? Investors appear concerned about:

- Flattish volume outlook with no visibility on tariff resolution

- Q1 2026 expected to be "the toughest quarter" on comparisons

- ~$300 million of identifiable headwinds (capital credits, taxes, other income)

- Continued mix pressure from weak high-margin segments

Industry Consolidation Commentary

Management addressed the proposed Union Pacific–Norfolk Southern merger, calling the STB's deeming of the filing as incomplete "expected" . Tracy Robinson was notably skeptical :

"It is not at all clear that the transaction, as proposed, addresses many of the questions around the negative impact on competition, as well as the bigger issue of increasing rail competition. The concessions required to achieve this will be significant."

CN incurred $15 million in advisor fees related to industry consolidation in Q4 . Management indicated that while the process plays out, the "majority of our team remains focused exactly where they should be, on running our business" .

Forward Catalysts

Near-term (Q1-Q2 2026):

- USMCA review timeline with July as key milestone

- Potential aluminum tariff relief as U.S. inventories deplete

- Gemini service expansion at Prince Rupert

- Q1 expected to be softer, improving through year

Medium-term (2H 2026+) :

- Phase 2 Greater Toronto Area Fuel Terminal

- New fractionators and crude oil expansion projects

- CanExport facility ramp-up (grain, plastics exports)

- Intermodex import transloading facility at Rupert

- Potential improvement in China canola trade relations

Beat/Miss History

*Values retrieved from S&P Global

CN has beaten EPS estimates in 5 of the last 8 quarters. The company's beat rate has improved in recent quarters following operational improvements and cost discipline.

Related Links: